The credit company that went too far. Would you let them invade your privacy?

On Sesame Credit and its including of social aspects into its social credit system

Sesame credit (also known as Zhima credit), a Chinese social credit scoring company, is now scoring people by taking account of their social interactions, and is intertwining the financial and social aspects of life. This is creating inequality in society by forcing people to use their apps, exercising control over people’s friend choices, enlarging the gaps among different social classes and the gap between people who have different e-literacies.

My experience with Sesame Credit Score

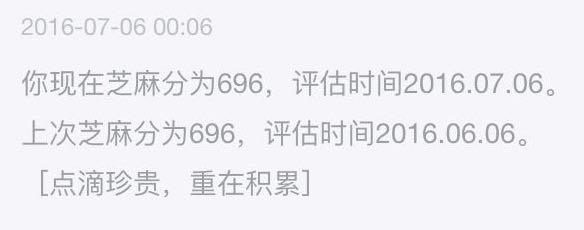

Starting in the beginning of 2015, Sesame credit is an independent third-party credit information company that belongs to the same group Alipay belongs to: Ant Financial Services Group (an affiliate of the Chinese Alibaba Group). Sesame credit is also one of the eight companies that has gained governmental permission and a business license to start its personal credit information service. The way to access one’s Sesame credit is through the Alipay app as they share the same account where one’s ID information is verified. According to Alipay, till the end of 2016, it has 450,000,000 verified accounts. Until March 23rd, 2017, using a Sesame credit score to avoid having to pay a deposit for using different services, such as renting a room, a bike or staying in an Airbnb, from different companies is available in 381 Chinese cities and around 20 million people have used such services. Last June (2016), I opened the Sesame credit score service and at that time my Sesame score was 696, as is shown in figure 1.

Figure 1. The Record of My Sesame Credit Score

Back then, I did not know much about how Sesame credit works out the scores for everyone and what would be the impact of it on my life. I knew my score was quite alright, because I used the Chinese e-wallet Alipay a lot. Sesame credit has access to my Alipay data, which includes all my online shopping records and offline consuming records in Alipay such as hailing taxis and paying for restaurant bills. It is also possible to prevent Sesame credit from accessing your Alipay data. Since last summer, I have seldomly used Alipay. So when I checked my Sesame credit the other day, I found it was more or less the same as it was last June, as is shown in figure 2.

Figure 2. My Sesame Credit Score

The aspects Sesame Credit Score takes into account

Figure 3. The aspects account for the Sesame credit score

I wondered why the growth of my Sesame credit score was so slow. By looking at figure 3, I found five aspects that account for one's Sesame credit score. They are your identity traits, compliance history, credit history, personal network and purchasing preferences. The aspects that raise scepsis are: personal network, purchasing preferences and identity traits.

The more high credit friends one's got, the higher one’s Sesame credit will be.

With regards to one's personal network, the Sesame credit algorithm is scoring a person's credit by calculating his orher friends' credit scores, which means the more high credit friends one has got, the higher one’s Sesame credit will be. This rule is actually limiting our choice of friends online. Besides, people who refuse using Alipay or who aren't e-literate will get low or no Sesame credit scores. I think it is very likely that these people will be discriminated and excluded by the larger part of society. After all, no one wants to make friends with people who have low reputation scores (even if they're digital scores).

The second aspect, the personal purchasing preference, contains too much shopping data, which raises some concerns regarding privacy. Online purchasing preferences have nothing to do with one’s trustworthiness. On the contrary, including this aspect is only good for surveillance.

What's more, the fact that personal identity traits are also considered when scoring is something that concerns people a lot. Giving everyone a single score according to these personal traits will definitely enlarge the gap between different social classes. As the higher social classes have higher Sesame credit scores, they can continously enjoy more privileges in this digital age, which will create more social inequality. It is possible to refuse to give out personal information, such as the highest education, job, property and car information, the temptation of completing your account in order to get a higher Sesame credit score and to make use of more services is becoming larger.

It should be all of our concern that with the prevalence and development of Sesame credit, people will be forced to use it out of social pressure.

The future development of Sesame Social Credit System

Right now, Sesame credit company is the only credit scoring company in China that connects individuals’ financial records with their social lives, which is dangerous. It should be all of our concern that with the prevalence and development of Sesame credit, people will be forced to use it out of social pressure. Moreover, if one day in the near future it is integrated with the crediting system controlled by the bank of Chinese (the official credit system for every Chinese citizen), everyone would only care about their social credit score and lose their genuine attitudes toward life. Since the crediting system is very new in China, not all citizens know how it works and not all citizens care about the data policies. If we do not care about this and people are allowing the company to do this, eventually, the tragic society depicted in the first episode of Black Mirror season 3 will come to Chinese society soon, "where the Uber-style rating system is extended to every aspect of life" and the amount of likes you receive on social media means everything.

Figure 4. The Tragic Society Depicted in Black Mirror

References

赵小燕, 黄慧. 支付宝发布2016全民账单:71%支付笔数发生在移动端. Retrieved May 3, 2017

ZHIMA CREDIT. Retrieved May 3, 2017

芝麻信用披露全国城市信用地图 381城开启免押金模式. Retrieved May 3, 2017

Renshaw, D. 7 Chillingly Real Questions Asked In The New Black Mirror. Retrieved April 18, 2017